Entrepreneurs generally have a high risk tolerance and are often willing to take on various challenges to start a business. And according to Finder’s Consumer Confidence Index, about 28% of Americans plan to start a new business in the next 12 months, despite the risks. Although starting your new business has many challenges, financial risks are among the biggest. We’ll discuss the top three financial risks that entrepreneurs should keep in mind when embarking on business ownership.

Obstacles to financing

Entrepreneurs face many risks when seeking a loan for their business. These risks may influence your ability to obtain financing as well as the terms of the loan. However, entrepreneurs who have difficulty obtaining financing from a traditional business lender still have options. Some best loans without documents offering loans to borrowers with a credit score as low as 500 or a sales history of no more than three months.

Here are some of the most common difficulties you might encounter when applying for a business loan:

- Insufficient time in business. Many business loans require a specified period of activity to be approved, often two years. However, some business lenders may offer more flexibility with one-year in-business requirements.

- Entrepreneurs with poor personal or business credit histories may have more difficulty obtaining financing.

- Higher interest rates or stricter loan terms. Entrepreneurs with less than stellar credit or who seek alternative loans are typically offered higher interest rates and less favorable loan terms.

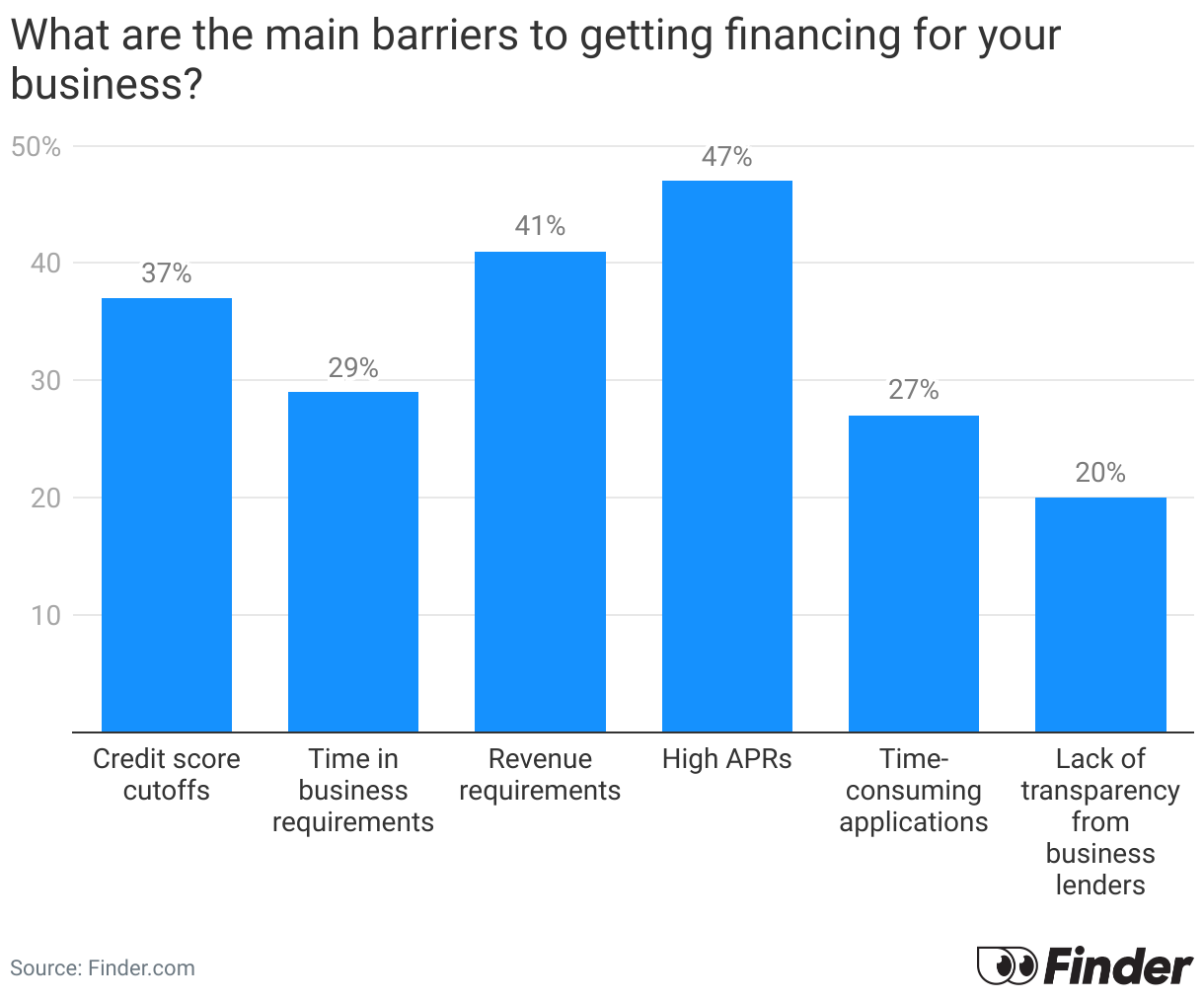

According to Finder Consumer Confidence Index, 42% of U.S. entrepreneurs agree that income needs are the main reason they can’t get financing for their business. This is followed by non-compliance with working time requirements, unaffordable APRs, time-consuming applications, non-compliance with solvency requirements and, finally, a lack of transparency.

Underestimating capital requirements

One of the most common financial risks entrepreneurs face is not having the funds they need to start or maintain their business. Entrepreneurs often invest their own money and seek funding from investors or borrow money to start their business. Underestimating the amount you need for start-up costs, unexpected expenses and the possibility of slower-than-expected revenue growth can mean running out of capital before your business becomes profitable. Make sure you develop a solid business plan with realistic financial projections that take into account unforeseen circumstances.

Market and economic fluctuations

New business owners are exposed to outside factors such as economic downturns, fluctuating market conditions and industry-specific challenges. A change in consumer behavior can negatively impact your sales and revenue, making it difficult to maintain profitability or keep within budget to repay outstanding business loans.

Conclude

Prepared and financially prudent entrepreneurs are better positioned to navigate these common financial challenges. Developing a solid business plan, securing the right level of financing, monitoring your cash flow, exploring alternative financing, and organizing information on industry trends can increase your chances of succeeding and sustaining your business.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.